Welcome to the world of VAT. It might not be the most thrilling topic, but it’s essential for businesses like ours. Let’s dive in and make sense of it together. Ready?

So, what exactly is VAT? Well, think of it as that sneaky little tax added onto most goods and services by businesses like ours. Introduced in the UK back in 1973, it’s now the government’s third-largest revenue source, trailing just behind income tax and National Insurance.

If you’re already up to speed with VAT and just here for insights into common VAT return mistakes, feel free to skip ahead. But if you’re still getting to grips with it all, let’s take a closer look.

Now, before you start feeling overwhelmed, let’s break down VAT into bite-sized pieces. Think of it as a puzzle, and we’re here to help you put the pieces together, one colourful block at a time.

What VAT rates are there?

Let’s explore the different VAT rates and exemptions to get a better understanding of how it all works.

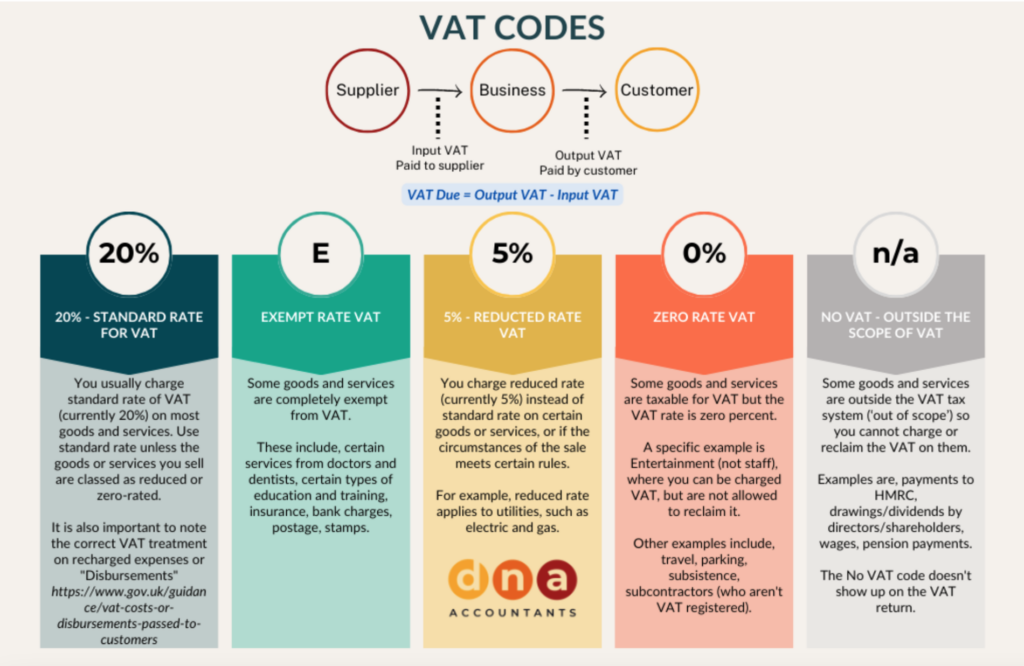

In the UK, VAT rates vary depending on the type of goods or services being sold. The standard rate is currently set at 20%, which applies to most goods and services. However, there are exceptions.

For certain items, a reduced rate of 5% may apply, such as on utility bills like electricity and gas. Additionally, some goods and services qualify for a zero-rate VAT, meaning they are still taxable but at a rate of 0%. This includes items like certain food items, children’s clothing, and books.

Furthermore, some goods and services are completely exempt from VAT altogether. These include necessities like medical services, education, and financial services.

While VAT-exempt items do not contribute to a business’s VAT liability, they still need to be carefully documented and accounted for in financial records. More info on specific examples can be found on the HMRC website.

Understanding which VAT rate applies to your goods or services is crucial for accurate tax calculations and compliance with HMRC regulations. It is also important to note the correct VAT treatment on recharged expenses or “Disbursements” View HMRC’s guidance here.

Now, let’s shine a light on an important VAT measure that specifically impacts the construction industry: the Domestic Reverse Charge VAT Rate.

For businesses operating in construction and related services, understanding the ins and outs of the Domestic Reverse Charge VAT Rate is crucial. It’s a measure aimed at combating VAT fraud within the industry while ensuring fair and transparent tax practices. More info can be found here.

What’s the VAT threshold in the UK?

Currently, the VAT threshold is set at £90,000. Once your total billed value gets close to or surpasses this magic number within a 12-month rolling period, it’s time to register for VAT. HMRC’s got some specific rules laid out for us:

You must register if:

- your total VAT taxable turnover for the last 12 months was over £90,000

- you expect your turnover to go over £90,000 in the next 30 days

A common misconception is that the “12-month rolling period” aligns with your financial year. However, it actually looks back at the previous 12 months regardless of your fiscal calendar.

Let’s say you run a small bakery. Over the past year, from April 2023 to March 2024, your total sales (VAT taxable turnover) amounted to £85,000. However, in April 2024, you notice a significant increase in orders, and you anticipate that your sales for the next 30 days will exceed £90,000.

Even though your sales for the past 12 months were below £90,000, because you expect to surpass this threshold within the next 30 days, you must register for VAT. HMRC considers both your past 12-month turnover and your anticipated turnover in the coming month when determining VAT registration requirements.

If you’re unsure about your VAT threshold or navigating VAT registration, feel free to reach out to us for guidance.

You must also register (regardless of VAT taxable turnover) if all of the following are true:

- you’re based outside the UK

- your business is based outside the UK

- you supply any goods or services to the UK (or expect to in the next 30 days)

Now, here’s where things get interesting: voluntary registration. Yep, you heard that right. You can choose to hop on the VAT bandwagon even if your turnover is below £90,000. Why, you ask? Well, there are perks! For starters, you can reclaim VAT on your business expenses, both now and retroactively. Plus, having that VAT number can give your business a professional edge and attract other VAT-registered partners.

But hey, we get it. Every decision comes with its pros and cons. If you’re on the fence about voluntary VAT registration, don’t sweat it! Give us a shout, and we’ll help you figure out what’s best for your specific needs.

How to register for VAT?

The information you’ll need to register for VAT depends on the type of your business. Most businesses opt for online registration, which streamlines the process and gets you on your way faster. Once you’ve submitted your application to HMRC, within approximately 30 days (though it could take a bit longer), you’ll receive a letter confirming your successful registration and, most importantly, your unique 9-digit VAT number.

From here you will then be able to log into your government gateway portal (or set one up) and download your VAT certificate. This will detail the effective date of VAT registration and the dates of the period for your first VAT submission that HMRC will be expecting.

Before you start slapping VAT onto your invoices, there’s one crucial detail to remember: you can’t do that until you’ve got your VAT number in hand. However, you can adjust your prices to accommodate the VAT you’ll need to pay to HMRC or issue a Pro-Forma VAT-inclusive invoice (though a full VAT invoice must be issued within 30 days). It’s all about keeping things above board and staying on the right side of the taxman.

How do you calculate VAT & charge it to customers?

When you sell goods or services, you must do the following:

1. Calculating VAT: Determine the total price including VAT by multiplying the price before VAT by 1.2 for the standard 20% rate.

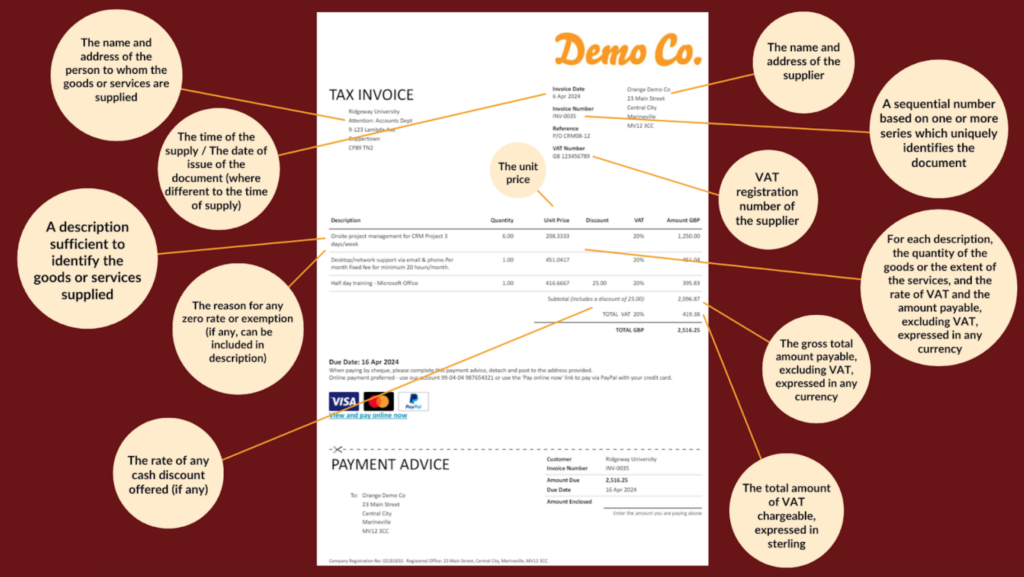

2. Invoicing: Ensure your invoices clearly show the VAT amount separately and include your VAT number – see a more detailed layout below

3. Recording Transactions: Log all transactions in your digital VAT account, as required by Making Tax Digital (MTD) regulations since April 2022. Xero is fully compliant with MTD, making it an excellent software choice for this purpose.

4. VAT Returns: Record the total VAT amount on your VAT return to comply with HMRC regulations.

Regarding when not to charge VAT, remember that certain goods and services are exempt. Even if you sell or buy an exempt item, you still need to record the transaction, but using a different VAT rate. Exempt items include financial services, property, education, healthcare, charity events, and more. Read the full list of VAT-exempt goods.

What is a VAT Reclaim and what is a valid VAT invoice?

A reclaim is where you claim back the VAT element on items you buy for use in your business. To do this, you must have a valid VAT invoice. If any items are also for personal use, you can only claim the business proportion of the VAT. You must keep records to support your claim and show how you arrived at the business proportion for a purchase.

There are different rules if your organisation is VAT-exempt (for example, an educational academy or an eligible charity). Read guidance on reclaiming VAT as an organisation not registered for VAT (VAT126).

You must show the following details on any VAT invoices you issue:

Special rules apply to invoices issued under a margin scheme or subject to a reverse charge. You need to follow the rules for such supplies.

If a supplier issues you an invoice where the amount to pay is wrong, you need to ask the supplier to correct it and issue a new invoice. If you pay less than the amount due on an invoice, you can only reclaim the VAT on the amount paid – not what is on the invoice. You cannot claim more VAT than is shown on a valid VAT invoice. So it is always worth double-checking the amounts.

TOP TIP: If you would like to check if a company is VAT-registered and using the correct VAT number you can use this link from gov.uk

Purchases before registration?

You’re eligible to reclaim VAT paid on goods or services purchased before your VAT registration if you bought them within specific timeframes:

- 4 years for goods (stock) you still have or goods that were used to make other goods you still have

- 6 months for services (EG: Accountants Fees/ Marketing/ IT/ Consultancy etc)

However, there’s a catch: you can only reclaim VAT on purchases made for the business that’s now registered for VAT. These purchases must serve a “business purpose,” meaning they relate to VAT-taxable goods or services you supply.

In essence, you can reclaim VAT on qualifying purchases made within the specified timeframes, as long as they directly contribute to your VAT-registered business activities.

What are the different types of VAT Schemes?

The two most common VAT schemes (methods of VAT calculation) are Cash and Accrual.

An ‘Accrual Scheme’ means that any bills you receive in the VAT return period (usually quarterly) and any sales raised (regardless of whether they have been paid or not) will be included. This is the standard VAT accounting scheme and the one most people will automatically be enrolled into.

A ‘VAT Cash Accounting Scheme’ means that your VAT is paid (sales) and reclaimed (purchases) on anything you have physically received into your business or paid out. This disregards the invoice date. You can only use cash accounting if your estimated VAT taxable turnover is £1.35 million or less in the next 12 months. This can be a much better option if cash flow is a problem.

Alternative VAT schemes include:

- Lets you work out what you owe HMRC in VAT as a percentage of your gross turnover.

- You can only use this scheme if you’re a small business with an annual taxable turnover of £150,000 or less excluding VAT.

- The amount of VAT you pay depends on your industry and type of business.

- Complete one VAT return each year instead of 4

If you are a retail business or sell second-hand goods, you may be able to use:

- Pay VAT on the value you add to the goods you sell rather than on the full selling price of each item

- Calculate the VAT once with each VAT return rather than calculating it for each sale you make

These schemes offer flexibility and cater to different business needs and circumstances. It’s essential to research each option thoroughly to determine which best suits your business. If you need guidance or advice, don’t hesitate to reach out for support.

What to include in a VAT Return?

You’ll need to include:

- your total sales and purchases

- the amount of VAT you owe

- the amount of VAT you can reclaim

- the amount of VAT you’re owed from HM Revenue and Customs (HMRC) (if you’re reclaiming VAT on business expenses)

To streamline the process and ensure compliance, consider using software like Xero to prepare your VAT return. This software can help alleviate the stress of record-keeping and ensure accuracy.

HMRC may check your records to make sure you’re paying the right amount of tax. This is called a VAT inspection. As long as you have all the necessary documentation listed below you will have no problem dealing with your VAT inspection.

You must keep a record of the following:

- everything you buy and sell (including zero-rated, reduced and VAT-exempt items)

- copies of all invoices you issue

- all invoices you receive (original or electronic copies)

- self-billing agreements (where the customer prepares the invoice)

- the name, address and VAT number of any self-billing suppliers

- debit or credit notes

- any goods you give away or take from stock for your private use

Additionally, keep general business records such as bank statements, cash books, cheque stubs, paying-in slips, and till rolls up to date.

When is my VAT due?

The deadline for submitting your return online is usually one calendar month and 7 days after the end of an accounting period. This is also the deadline for paying HMRC. Ensure you allow sufficient time for your payment to reach HMRC’s account. If you are unsure you can use the HMRC VAT payment deadline calculator.

Missing the submission deadline prompts HMRC to issue a ‘VAT notice of assessment of tax,’ informing you of the estimated VAT owed. Late submissions or payments may incur surcharges or penalties, the amount of which varies depending on your accounting period.

You should contact HM Revenue and Customs (HMRC) as soon as possible if you’re having difficulty paying by the deadline.

Failure to report and pay the correct amount of VAT may result in HMRC charging interest. However, if HMRC mistakenly overcharges you, you have the right to claim interest on the excess payment.

Late submissions of VAT returns accrue penalty points, including nil returns. Once you reach your penalty point threshold, you’ll incur a £200 penalty. Additional £200 penalties apply for each subsequent late submission while at the threshold. You can monitor your penalty points in your online HMRC account.

What if I paid out more VAT than I charged my customers?

If you find yourself in a situation where you’ve paid out more VAT than you’ve charged your customers, HMRC typically reimburses you the difference.

Repayments are normally processed within 30 days of HMRC receiving your VAT Return. If you haven’t received any communication from HMRC after this period, it’s advisable to chase this up.

The repayment is usually deposited directly into your bank account if HMRC has your bank details on file. However, if they don’t have this information, HMRC will issue a cheque, also known as a ‘payable order.’

Errors in your VAT Return

Now, onto everyone’s favourite topic: VAT returns. We’ve all been there, staring at those daunting forms, wondering if we’ve made a mistake somewhere. But fear not! We’ve compiled a list of common blunders, from using the wrong tax rate to letting the AI take the wheel (spoiler alert: it’s not always right).

One of the most common errors I frequently encounter when reviewing VAT returns is the incorrect application of tax rates to items. Many individuals tend to assume that the tax rate is either 20% VAT or no VAT. While technically this is correct, opting for the “No VAT” tax rate can sometimes lead to misplacement of your transaction in the wrong box of the return.

In addition to the misuse of tax rates, several other recurring issues often arise during VAT return reviews. These include:

1. Wrong COA code usage: Using incorrect Chart of Accounts (COA) codes can lead to misclassification of transactions, resulting in errors in reporting and analysis. A common fault is posting to a balance sheet code, rather than the profit and loss code.

2. Posting small amounts to fixed assets: Inappropriately categorizing small expenses as fixed assets can distort financial statements and skew performance metrics. As a rule of thumb, we tend to only capitalise expenses over £250 (although there can be exceptions to this rule).

3. Forgetting to check what you owe: If you don’t double-check what you owe (like bills or loans), you might not report all your debts accurately. This can make your financial statements wrong and cause problems down the line. It’s important to regularly review what you owe (found on your balance sheet) to make sure your financial records are correct.

4. Double coding through both cash and bills/invoices: Posting the same transaction multiple times, such as through both cash coding and adding the invoices, can lead to duplicate entries. A quick review of the outstanding bills and invoices can help to reduce this error.

5. Incorrect completion of the “Who What Why” boxes in Xero, sometimes relying too heavily on AI: Sometimes, people don’t fill in the “Who What Why” boxes properly in Xero. A common issue is incorrectly recording bank transfers between accounts as direct postings to a COA instead. Also, depending too heavily on AI to do this for you can lead to errors in your records. As Xero gets smarter, more suggestions are being made during reconciliation. It’s essential to make sure these details are accurate for proper financial tracking.

6. Forgetting to review the VAT return report: Sometimes, people don’t take a second look at the VAT return report before submitting it. This can lead to missing errors or inaccuracies in the report. It’s essential to double-check everything to ensure accuracy as it’s easy to code things wrong if you are in a rush!

Each of these problems highlights how important it is to pay close attention to details and use good accounting practices. This helps make sure your financial reports are accurate and that you follow the rules correctly.

Correcting errors in your VAT Return?

If you make mistakes in your VAT Return, you can fix them within the past four years if they’re:

- £10,000 or less

- Between £10,000 and £50,000, but less than 1% of your total sales value

For these kinds of errors, you can just correct them in your next VAT return.

However, if the errors are:

- Over £50,000

- Over £10,000 and more than 1% of your total sales value

- Deliberate mistakes

You need to tell HMRC separately about them.

For more information on VAT from HMRC, please visit their website.

In conclusion, VAT comes with a lot of rules and regulations, and it’s easy to get lost in the details. If you’re unsure about the right approach, don’t hesitate to reach out to us. We’re here to help you navigate through the complexities and ease your worries. And if you’re considering handling your own VAT returns, be sure to check out this blog for valuable insights before diving in.