If you’re in the building trade and you’ve ever scratched your head wondering why 20% got taken off your invoice — or whether you’re supposed to register with HMRC — you’re in the right place.

We’ve put together a friendly, plain-English guide to the Construction Industry Scheme (CIS) that explains everything without the jargon. Whether you’re a sole trader, limited company or somewhere in between, here’s what you need to know — in real-world language that actually makes sense.

What even is the Construction Industry Scheme (CIS)?

CIS is HMRC’s way of collecting tax from the construction sector, where lots of tradespeople are self-employed. Under the Construction Industry Scheme (CIS):

- Contractors deduct tax from subcontractor payments and send it to HMRC.

- Subcontractors have tax deducted before they’re paid, unless they’re registered for gross payment status.

It’s a way to keep the tax system ticking — and if you’re in construction, chances are it applies to you.

Does CIS apply to me?

Here’s the quick and dirty checklist:

CIS covers:

- Most construction work in the UK

- Sole traders, partnerships, limited companies — even public sector bodies

- Building, decorating, groundwork, demolition, repairs, system fitting and more

CIS doesn’t cover:

- Private homeowners getting work done

- Jobs outside the UK

The CIS guide for contractors and subcontractors has more details on what is and is not covered by the scheme.

Are you a contractor, subcontractor, or both?

Let’s simplify:

- A contractor pays others to carry out construction work.

- A subcontractor is paid to do that work.

Plenty of businesses are both. Maybe you’re hired by a main contractor to do a job, but you’ve also got a team of subbies you bring in to help. If that sounds like you, congratulations, you get to wear both hats under the Construction Industry Scheme (CIS).

That means you’ll need to:

- Register as both a contractor and a subcontractor

- Deduct CIS from your subcontractors

- Suffer CIS deductions from your own payments

The good news? HMRC lets you offset the CIS that’s been deducted from you against the CIS you’ve deducted from others.

Here’s how it works:

Let’s say:

- You’ve had £500 deducted from your own payments as a subcontractor

- You’ve deducted £800 from your own subcontractors

Instead of sending £800 to HMRC, you can offset the £500 already deducted from you, and just pay the £300 balance to HMRC.

This offsetting happens before you make your monthly payment to HMRC, and it helps keep your cash flow steadier, especially if you’re regularly juggling both roles.

Need help tracking all this? That’s exactly the kind of thing we sort for you.

How to register for CIS

Contractors:

- Must register with HMRC before paying their first subcontractor.

Subcontractors:

- Should register before starting any work to avoid 30% deductions.

You can do it online or ask your accountant (like us!) to sort it.

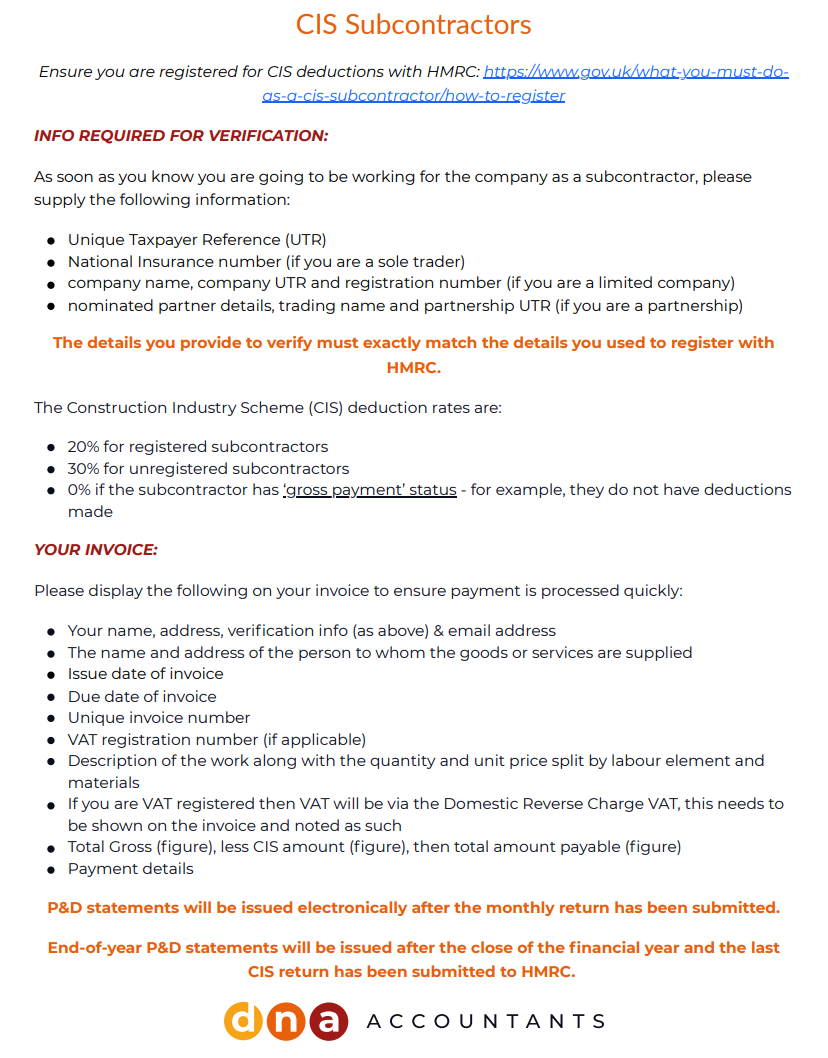

How subcontractors get verified & paid

There are three ways HMRC allows subcontractors to be paid under CIS:

- Gross – you’re paid in full with no tax deducted (only available if you apply and qualify (check this out here)

- Standard – 20% is deducted from your labour charges if you’re registered

- Higher – 30% is deducted if you’re not verified with HMRC

Before making a payment, contractors must verify you with HMRC. This check confirms which deduction rate applies. If the contractor can’t verify you, then CIS rules say they must deduct tax at 30% by default.

Each time you’re paid, your contractor must issue a Payment & Deduction (P&D) statement. This shows the amount paid to you, how much tax was deducted under CIS, and the period it relates to.

📝 You are legally entitled to receive these statements.

If you haven’t received one by the 19th of the following month, you should request it from your contractor — they are required to provide it once their monthly CIS return has been submitted.

To make sure your payments go through without delays, it’s essential that your invoices are accurate and contain the correct information.

We’ve pulled together a quick reference list of what to include in your invoices:

Save it somewhere handy, or print it out and keep it near your invoice template!

What does the CIS deduction apply to?

One of the biggest misunderstandings we see with CIS is what the deductions actually apply to. Let’s clear that up:

- CIS only applies to the labour element of an invoice.

That means if you’re charging for both your time and materials (like tools, fixings, or supplies), the deduction is only made on the labour bit.

Here’s a quick example:

Let’s say a subcontractor invoices for:

- £1,000 labour

- £300 materials

- £260 VAT (20%)

Even if CIS applies at 20%, the deduction is only taken from the £1,000 labour. So in this case:

- 20% of £1,000 = £200 CIS deduction

- The contractor still pays the £300 for materials and accounts for the VAT separately (via the Domestic Reverse Charge if it applies)

So the total paid to the subcontractor would be:

£1,000 + £300 – £200 = £1,100.00 (DRC VAT of £260.00 accounted for separately)

Pro tip: Always clearly split labour and materials on your invoices — it avoids confusion, delays, and incorrect deductions.

If you’re VAT-registered, don’t forget to also show the correct Reverse Charge VAT wording – more on this below.

A quick word on VAT and the Domestic Reverse Charge (DRC)

If both you and your subcontractor are VAT-registered and working in the construction industry, the Domestic Reverse Charge (DRC) may apply. This rule shifts the responsibility for accounting for VAT from the subcontractor to the contractor.

Here’s how it works:

- Instead of the subcontractor charging and collecting VAT on their invoice, they show “Reverse charge: VAT Act 1994 Section 55A applies”.

- The contractor then accounts for both the output and input VAT on their VAT return — no actual money changes hands.

- The VAT rate used under DRC is still 20%, but it’s reported, not paid.

Why it matters: If you’re using CIS and the DRC applies, it changes how you handle VAT, but not how you apply CIS deductions. You still deduct CIS on the labour part of the invoice, just like normal.

It can be a headache, so if you’re not sure whether DRC applies to you, shout — we’ll sort it.

Monthly contractor duties

Each month, you must:

- Submit a CIS return for the period 6th to 5th

- Include all payments during this period (or submit a ‘nil’ return if there haven’t been any)

- Pay HMRC by the 19th (or 22nd if online)

You must check if you should employ the person instead of subcontracting the work. You may get a penalty if they should be an employee instead.

Tax for subbies: What happens to the deductions?

Being under CIS doesn’t mean you don’t need to file a return.

Subcontractors still file Self-Assessment returns (or company accounts). They can use their CIS deductions to reduce their tax bill

Limited companies can offset these deductions against PAYE and NI, and claim a refund if they’ve overpaid.

Note that if you are claiming an overpayment HMRC will use this money to offset any other HMRC liabilities – EG Corporation Tax and VAT!

Common CIS questions

Q: I’ve been told I’m a subcontractor — does that mean I’m self-employed?

Yes, usually. If you’re working under CIS, HMRC treats you as self-employed for that job. That means you’ll need to keep records and file a Self Assessment tax return — even if it’s just one-off work.

Q: Do I have to register for CIS as a subcontractor?

Technically, no — but if you don’t, your contractor will deduct 30% from your payments instead of 20%. Registering means you keep more of your money now and settle the rest at year-end. It’s a no-brainer really.

Q: What if I don’t include the right info on my invoice?

It could delay your payment, or worse, result in the wrong CIS deduction. Make sure your invoices clearly split out labour and materials, show your UTR, and include the correct reverse charge VAT wording if needed. Use our invoice checklist PDF to get it spot on.

Q: Can I offset CIS deductions against my tax bill?

Yes! If you’re a sole trader, those deductions go towards your Self Assessment bill. If you’re a limited company, you can offset them against your PAYE and NI and reclaim anything left over.

Q: I’m a contractor but only hire people occasionally — do I still need to register?

Yes, even if it’s just a few jobs a year. If you’re paying subcontractors for construction work, you’re classed as a contractor and need to register with HMRC.

Q: What happens if I stop using subcontractors for a while?

You can submit a ‘nil return’ each month to let HMRC know – this keeps you compliant without submitting full details. Don’t just ignore it, though — you could still get fined.

Q: What’s the difference between PAYE and CIS?

PAYE is for employees. CIS is for subcontractors. If someone works under your direction and control (like set hours, using your tools, and can’t send a substitute), they may be an employee, and you should check their employment status properly.

Q: Can a subcontractor also be VAT-registered?

Yes! And if they are, they’ll likely need to use the Domestic Reverse Charge VAT. That means they don’t add VAT to their invoice — instead, the contractor accounts for it. Don’t forget to include the correct wording on the invoice.

Penalties to avoid

- Late filing = automatic £100 fine

- Incorrect verification = penalty

- Poor records = up to £3,000 fine

Keep things clean, consistent and on time — or HMRC will come knocking.

Need help with CIS?

Whether you’re a contractor, a subcontractor, or both, we make the Construction Industry Scheme (CIS) easy. From registrations to monthly filings, our team keeps you compliant, efficient, and penalty-free.